But that might increase Fed officials' concerns about a market bubble that eventually pops, Bostjancic states." it's a close call," Bostjancic states. She, as well as economic experts at Goldman and JPMorgan Chase, expect the Fed to move the bond purchases to trim rates while Nomura, Barclays and Morgan Stanley predict the Fed will stand pat.

Rates are currently traditionally low and the real estate market is expanding. A shift in the Fed's mix could lower home mortgage rates by about 15 basis points, lowering the monthly payment on a $200,000 home loan by $15, or $180 year, states Tendayi Kapfidze, chief economist of Providing Tree. Lots of financial experts are more confident the Fed will offer more particular assistance on how low long it will continue to purchase bonds.

Goldman Sachs believes the Fed will say it will keep purchasing bonds at the existing speed till the labor market is "on track" to reach full employment and inflation is "on track" to reach 2%. That's similar to the Fed's criteria for raising its crucial short-term rate however not as rigid.

Bostjancic states Fed officials likely wish to prevent another "taper temper tantrum" a 2013 spike in Treasury yields when Fed authorities all of a sudden indicated they would begin unwinding bond purchases following the Great Recession of 2007-09. Likewise, investors now anticipate the Fed to begin tapering the bond purchases in late 2021 or early 2022.

Alexander, though, says the Fed may wait up until the outlook is clearer prior to fine-tuning its guidance. In September, the Fed forecasted the economy would contract 3. 7% this year and unemployment would end the year at 7. 6%. But the economy has recovered from the pandemic more promptly than anticipated, with unemployment currently at 6.

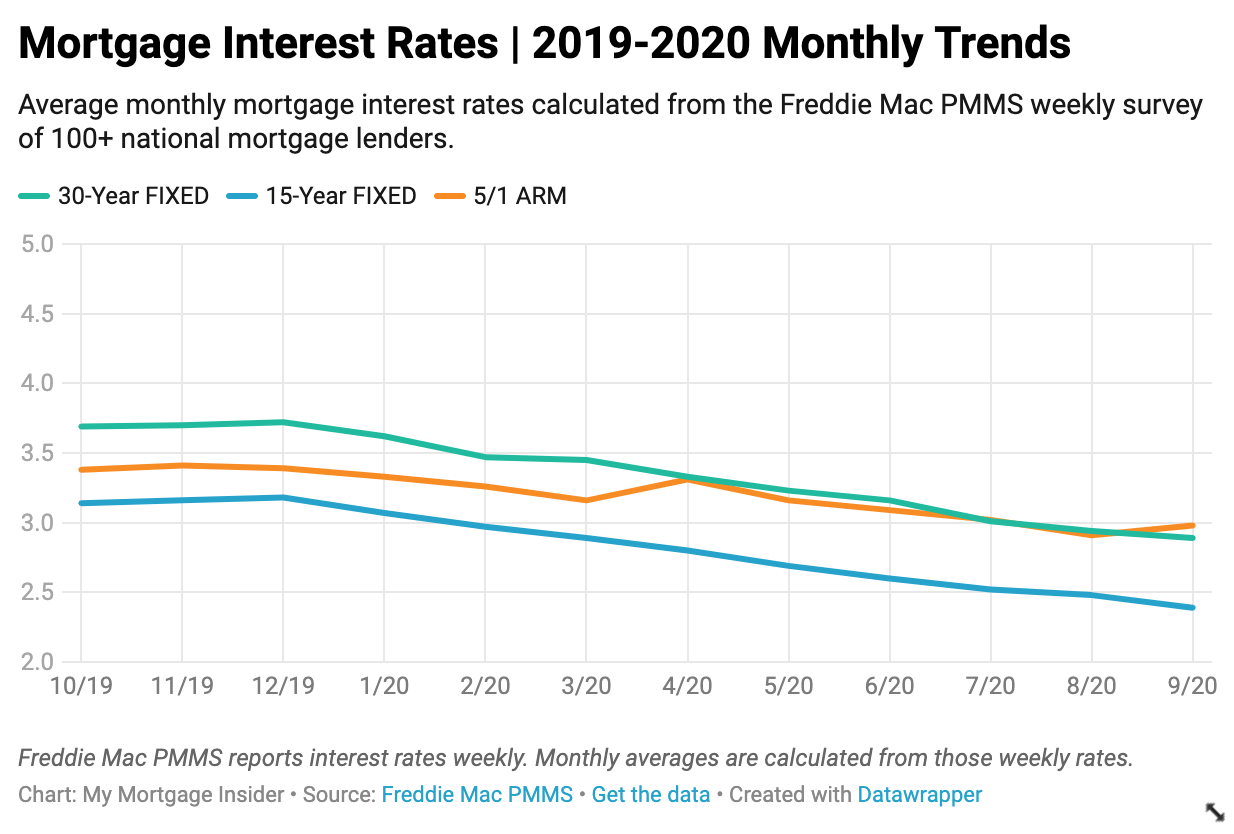

See This Report about What Are Current Interest Rates For Mortgages

Goldman Sachs anticipates the Fed to modify its forecast to a 2. 5% contraction this year and unemployment of 6. 8% at year-end. Goldman also anticipates the Fed to modestly raise its price quote of financial development next year to 4. 2%, up from its prior projection of 4%. Oxford, however, reckons the Fed will decrease its price quote for next year as the results of the virus spike exceed the increase from the vaccine.

Shopping around for a mortgage or home mortgage will assist you get the best funding offer. A mortgage whether it's a house purchase, a refinancing, or a home equity loan is a product, much like a car, so the cost and terms may be flexible. You'll want to compare all the costs associated with getting a home loan.

Obtain Information from Numerous Lenders Obtain All Crucial https://www.ktvn.com/story/43143561/wesley-financial-group-responds-to-legitimacy-accusations Expense Information Mortgage are readily available from a number of types of lending institutions thrift organizations, business banks, home mortgage business, and credit unions. Different lenders may quote you different prices, so you ought to get in touch with several lenders to make sure you're getting the very best rate. You can likewise get a mortgage through a mortgage broker.

A broker's access to numerous lending institutions can mean a broader selection of loan items and terms from which you can pick. Brokers will normally call a number of lenders concerning your application, but they are not obliged to discover the very best deal for you unless they have contracted with you to function as your representative.

Whether you are handling a loan provider or a broker may not constantly be clear. Some financial organizations operate as both loan providers and brokers. And most brokers' ads do not use the word "broker." For that reason, make certain to ask whether a broker is included. This information is important since brokers are normally paid a cost for their services that might be different from and in addition to the loan provider's origination or other charges.

The Definitive Guide to When Did 30 Year Mortgages Start

You must ask each broker you deal with how she or he will be compensated so that you can compare the various costs. Be prepared to negotiate with the brokers in addition to the loan providers. Be sure to get info about home loans from several lenders or brokers. Know just how much of a deposit you can manage, and find out all the expenses included in the loan.

Request for information about the very same loan amount, loan term, and type of loan so that you can compare the details. The following details is necessary to get from each loan provider and broker: Ask each lending institution and broker for a Click here for more info list of its present home mortgage rates of interest and whether the rates being estimated are the most affordable for that day or week.

Bear in mind that when rates of interest for variable-rate mortgages go up, generally so do the monthly payments. If the rate estimated is for an adjustable-rate home mortgage, ask how your rate and loan payment will vary, consisting of whether your loan payment will be decreased when rates go down. Inquire about the loan's interest rate (APR).

Points are costs paid to the lending institution or broker for the loan and are typically connected to the rates of interest; usually the more points you pay, the lower the rate. Check your local paper for information about rates and points presently being offered. Request for points to be priced quote to you as a dollar amount rather than just as the number of points so that you will understand just how much you will in fact need to pay.

Every lending institution or broker need to be able to offer you an estimate of its charges. Many of these charges are negotiable. Some costs are paid when you look for a loan (such as application and appraisal fees), and others are paid at closing. In many cases, you can borrow the cash required to pay these fees, however doing so will increase your loan quantity and overall expenses.

The smart Trick of What Is The Interest Rate For Mortgages Today That Nobody is Discussing

Ask what each charge includes. A number of items might be lumped into one cost. Ask for a description of any fee you do not understand. Some common fees related to a home mortgage closing are listed on the Home mortgage Shopping Worksheet. Some loan providers need 20 percent of the house's purchase cost as a down payment.

If a 20 percent deposit is not made, lenders normally require the homebuyer topurchase private mortgage insurance coverage (PMI) to secure the lending institution in case the homebuyer fails to pay. When government-assisted programs like FHA ( Federal Real Estate Administration), VA (Veterans Administration), or Rural Development Services are readily available, the down payment requirements might be considerably smaller sized.

Ask your loan provider about special programs it may offer. If PMI is required for your loan Ask what the overall expense of the insurance will be. Ask just how much your month-to-month payment will be when the PMI premium is included. When you know what each lender has to provide, work out the best deal that you can. how do mortgages work in canada.

The most likely reason for this distinction in rate is that loan officers and brokers are typically allowed to keep some or all of this difference as additional payment. Normally, the distinction in between the least expensive available rate for a loan item and any greater price that the debtor consents to pay is an overage.